I wrote a post last year applauding them on their policy announcement on products from Israeli settlements. I also pointed out that the Co-op and its Bank seemed to be the only one that remembered its origins and retained its ethical stance. That's why I'm a customer.

I'm disappointed that the Co-operative Group and the Co-op Bank are not behaving in a manner consistent with its 'customer led, ethically guided' public policy.

It seems as if individuals are suddenly popping up on websites to challenge the work of Mark Taber and the Co-op Bank Action group, attempting to scare bondholders and preference shareholders. I'd be very very sad and disappointed if it turns out that these people are connected with the Co-op Bank in some way and are part of a management strategy to deal with uncomfortable negative publicity.

The Financial Conduct Authority, one of the organisations that replaced the UK's FSA, has now given advice to customers who fear they may lose their Co-op investments.

The FCA is there to regulate conduct in relation to financial products. It has the power to investigate organisations and individuals.

The head of the FCA, Martin Wheatley, has effectively told Co-op bank investors that they're on their own. They must wait and see what Co-op bank decides to do to salvage its financial stability. He claims that Co-op bonds were inherently risky, that this was disclosed at issue and that any future loss should be dealt with by referring to the customer's financial adviser (presumably to sue them for misselling).

Mark Taber, of the Co-op Bank Action Group, disagrees. He and a group of energetic researchers have gathered data, which he's used to present a coherent argument to contradict Mr Wheatley's assertions. Taber has also assembled links to documents supporting his defence of customers. Mark has also gathered press cutting from 1992 covering the PIBS, which further debunk Mr Wheatley's claims.

Taber concludes by pointing out that a 13% coupon was not exceptional in 1992, when Government gilts (rock solid secure investments) were issued with a 12% coupon and annuity rates were 13-14%. Perhaps Mr Wheatley is relying on a younger, gullible readership, who have never experienced rates above 10%.

'Perhaps some of you IFAs would like to present this research to Mr Wheatley and ask why he is telling people to sue you?'

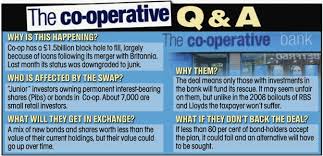

The Co-op Bank is in trouble. This institution was founded to help its members and run on ethical lines like the rest of Co-op Group.

Unfortunately senior management did not exercise due diligence. Money was lost and the bank was declared at risk by the authorities.

The Co-op Group will back the bank, but will not pay the debt. The plan is to scalp certain investments by Co-op Bank members (in a similar way planned by Bank of Ireland when it got into trouble.)

I was assured by a manager that I would not be affected. I hold an account with the bank, but neither bonds nor preference shares. I was also told that the offenders had left the bank and were not given a golden goodbye.

This member of staff then asked if I'd like to invest some of money I had in my current account. I replied that I planned to transfer everything above the limit guaranteed by the government, as I no longer trust Co-op Bank. The shocked look on this woman's face spoke volumes about the naivety of Co-op Bank. "But your account won't be affected. Why transfer?" I told her that I would act in solidarity with all the ordinary people who trusted Co-op bank for years and who were about to lose their life savings because of the mistakes made by senior management.

The Co-op Action Group is rallying support for those affected by the plan. Here is one comment by its founder:

'I get seriously angry when I receive letters from the children of vulnerable pensioners in their 80's and 90's who put all their nest egg in Co-op preference shares when they retired because, for some in that generation, the Co-op was a way of life (they banked, shopped, did business with the old Co-op Societies etc) and they trusted it implicitly. As above these preference shares should not be included. And this is coming from an organisation which prides itself on the following values:

Self-responsibility - we take responsibility for, and answer to our actions? Equity - we carry out our business in a way that is fair and unbiased? Openness - nobody's perfect, and we won't hide it when we're not? Honesty - we are honest about what we do and the way we do it?

Incidentally all the press stories which could cause a run on the Bank (which is the biggest risk of the resolution) such as resolution if bondholders do not agree to the Bank's plan, bonds being rendered worthless, Group debt covenants being fully stretched etc have been planted by the Co-op and not us. Makes you wonder what they really wants!'

Mark Taber has helped fixed income investors, who have had problems with other banks. He is now actively gathering information and ideas to rally support for those who fear the loss of their life savings.

Over the years I've had conversations with people about dietary changes that may improve health and weight. I can spot the slow, mocking smile that precedes a few typical comments.

'That's purely anecdotal evidence.' 'There's no research to support that view'.

I can cite research papers or wave books full of evidence in front of their faces, but it makes no difference.

Sometimes the speaker has a favourite guru such as Ben Goldacre. If he doesn't write about specific nutrition to address heart disease, then it's wrong.

Often I'm in conversation with a psychologist or psychiatrist who works with the health service. They betray interesting fixed beliefs and convoluted logic.

'I've never heard of it. The Department of Health advocates the opposite. Therefore this idea is wrong.'

'If this approach worked then all doctors would be using it.'

2 examples illustrate the limitations of this reasoning:

Ancel Keys concluded that a high fat diet led to higher rates of death from heart disease in 1956 based on the Seven Countries Study. It appears that the data was extracted from a 100 countries study. Keys selected 7 countries to support his hypothesis, when other countries contradicted it. This is known as confirmation bias.

Unfortunately Keys' report was used as the basis for government health recommendations on low fat high grain diets, which many believe to have contributed to obesity and rising rates of heart disease.

Joan Jerome went cold turkey after living a zombie-like life on 9 prescription drugs. She founded Tranx to help others come off minor tranquilisers and anti-depressants of the benzo family.

Her work was swiped and copied by media people and high profile doctors. They produced documentaries and books which included her list of side effects and symptoms, as well as treatment protocols. The organisation was successful in changing medical practice and prompting drug companies to develop the Prozac generation of anti-depressants. Every doctor with whom I've discussed withdrawal from benzos, repeats her protocols verbatim, as if some university researcher or pharmaceutical company had devised them. Joan Jerome is not credited with this work. Unfortunately people are still struggling with the effects of benzo addiction.

N = 1 or the use of self as a research subject is derided. Double blind studies are the gold standard, but rarely the starting point for any useful and testable hypothesis. Both Jimmy Moore and Seth Roberts use and encourage N = 1 experiments. Seth also favours checking the medical evidence for doctor's recommendations.

I've found that my scornful conversation partners have never investigated health matters and come up with their own hypothesis. Sadly they seem to believe governments or a single guru without question (or much thought.)

There's no clear definition of a low carb diet. The variants from Atkins to different versions of Paleo have a range of views on macronutrient ratios. They all have lower carb levels than SAD, the Standard American Diet.

Some, like a few Paleo flavours and Protein Power advocated by Michael & Mary Dan Eades, include high levels of animal protein.

Others like vet, Petro Dobromyskyj, of Hyperlipid advocate high fat levels.

Some variants of Paleo including the PHT, the Perfect Health Diet, allow 'safe starches' such as taro, sweet potatoes and rice.

Most seem to agree that all or most grains are unhealthy and should be avoided.

All seem to agree that fat and saturated fat are healthy and desirable. Most recommend avoiding industrial seed oils and margarine. Coconut and olive oil as well as butter are commonly favoured.

On many diets, not just low carb, people often report weight regain after a year or so. Some attribute this to slackness and deviation from guidelines. We may fool ourselves into thinking we don't eat a lot, when appetite has crept up.

Endocrinologist, Dr Robert Lustig commented that low carb diets are useful for weight loss, but are difficult to follow in the long term.

Jimmy Moore dismissed this until he begain to regain weight on his version of low carb, which at one stage involved consumption of red meat 3 or more times a day.

Dealing with weight regain is tackled in different ways depending on the initial health history of the author and/or their commercial interests in differentiating their particular diet.

Former doctors and current kitchen appliance vendors, the Eades, suggest that weight gain occurred when people had too much berry fruit and vegetables. They also advise women to reduce cheese consumption as this can sabotage weight loss efforts.

Heart surgeon, Dr Steven Gundry also suggests people eat less cheese, but strongly recommends a gradual reduction of animal protein to modest levels. He avoids cow's milk products and advocates goat's milk products.

Formerly obese, Jimmy Moore, now advocates a constant state of ketosis with high fat levels and regular ketone testing.

Jenny Ruhl, a diabetic who focuses on blood sugar control, advises people to measure and restrict calorie intake. She also comments on problems faced by menopausal women, where depleted oestrogen levels are associated with retention of belly fat. High fat intake may lead to weight gain. She quotes pioneer low carb treater of diabetes, Dr Richard Bernstein, who found that some health conditions, such as polycystic ovary syndrome could play havoc with blood sugar levels. He also noted that some forms of diabetes do not respond to dietary changes.

Researcher, Paul Jaminet, suggests that underlying health conditions may sabotage weight loss and health regain. He advocates investigation and treatment of parasites and gut problems.

A number of bloggers in the field, such as psychologist Seth Roberts, consider that weight gain/loss/maintenance depend on our set point. This metabolic 'fat thermostat' may be affected by the types of food we consume. They suggest that the set point drives hunger and weight gain unless we alter it. Seth Roberts suggests that flavourless foods can recalibrate the set point, as they are not associated with calories.

For me, it's not a question of how to lose weight initially.

People have lost weight on a variety of diets over time. High salad, moderate starch and low fat works well for some people.

The bigger issue is what to do if and when some of that weight is regained.

In my experience the initial tactics for weight loss may not work so well a few years down the line. As Jenny Ruhl says, this may be associated with changes as we age, particularly hormonally. Others suggest that our enzymes don't function as well in later life.